Financial regulation is often a complex issue for Swiss banks. The same applies to their lawyers and consulting firms. How can they combine a good level of compliance and risk mitigation, with real efficiency at work, when they’re running out of time? We believe that these professionals have everything to gain from adopting a RegTech regulatory search tool. Find out more in this article about the benefits and functionalities of this type of solution for the world of finance.

1 – Why is regulatory search often a pain point for banks?

The Swiss financial sector is complex. It comprises multiple layers of regulation. Laws, ordinances, FINMA circulars and self-regulation are essential elements of the Swiss regulatory landscape for banks. The texts overlap. They are subject to regular changes. Sometimes, for specific questions, financial services specialists need to study additional documents. These include explanatory reports and consultation reports. It’s often difficult to keep track of all this information.

1.1 – The complexity of multi-source, evolving financial regulation

One of the challenges faced by financial professionals in Switzerland is navigating the vast amount of text relating to financial regulation. Whether they emanate from the Swiss prudential authorities, the Basel Committee or European and international institutions, there are numerous sources to consult. Bank employees have to deal with thousands of pages of financial regulations.

From reporting and banking ratios, to risk management and regulatory changes, these financial professionals need to find the right information. The sheer volume of regulatory data requires an understanding of its structure. It also requires keeping abreast of new developments and changes with the various players involved in compliance.

1.2 – Challenge to quickly find the information you are looking for in the regulations

Without access to an effective research tool, these banking industry professionals find it challenging to find the right information quickly. How can they identify not only the relevant regulations, but also related legal documents (explanatory reports, consultation reports, etc.)?

1.3 – Numerous regulatory texts with a high cost of compliance

The large amount of information that needs to be consulted in order to apply the regulations to banks in Switzerland generates significant financial costs. All this time spent on regulatory research, without adequate tools, represents an expenditure of energy and therefore money. Add to this the risk of non-compliance due to misunderstanding or oversight, and the economic impact is even greater. Reducing these costs is a real challenge for the banking sector.

2 – The need for a RegTech-type regulatory research tool

To quickly find what you need in the regulations, with an up-to-date overview, while reducing risk, adopt a RegTech-type search tool.

2.1 – The need to rationalize document searches with a tool

To avoid having to manually search through many documents, professionals benefit from using an IT solution. It structures their work. This is the case when preparing documentation for special restatements, for example in view of upcoming vacations. It’s also a need within a banking department, or between collaborators in a consultancy firm who want to exchange information efficiently on a regulatory subject.

2.2 – Why use new RegTech technologies?

RegTech or Regulatory Technology refers to a set of IT applications that help banking organizations and the companies that advise them to comply with laws and regulations. These tools use Tech technologies such as automation, artificial intelligence and Big Data, generally in a cloud environment.

By adopting a Fintech tool specialized in regulation, it becomes possible to streamline searches and track relevant information for regular use. The services offered by RegTechs also make it possible to comment online on texts and share information within a team at a bank or law firm.

2.3 – Making regulations a working tool through structured research

RegTech to search in regulation is a powerful tool. The use of specialized applications in research speeds up the process and increases accuracy. In fact, investigations cover not only the regulations themselves, but also related documents such as explanatory or consultation reports.

What’s more, a regulatory search tool reduces work time by allowing specific keywords or phrases to be entered into an engine. Bank employees no longer have to manually scour several documents or websites. With RegTech, searching for information finally becomes fast and convenient. You reduce the complexity of financial regulation.

RegTech solutions work with constantly updated documentation. They are online research tools. This means you always have an up-to-date overview of regulatory information. And let’s not forget that future regulations are also displayed.

2.4 – Reducing risk with RegTech regulatory research

Having access to an efficient search tool when working with Swiss financial regulations has many advantages. Financial professionals dealing with Swiss regulations can locate relevant information faster and more accurately. The result is a streamlined workflow that helps reduce the risk of non-compliance.

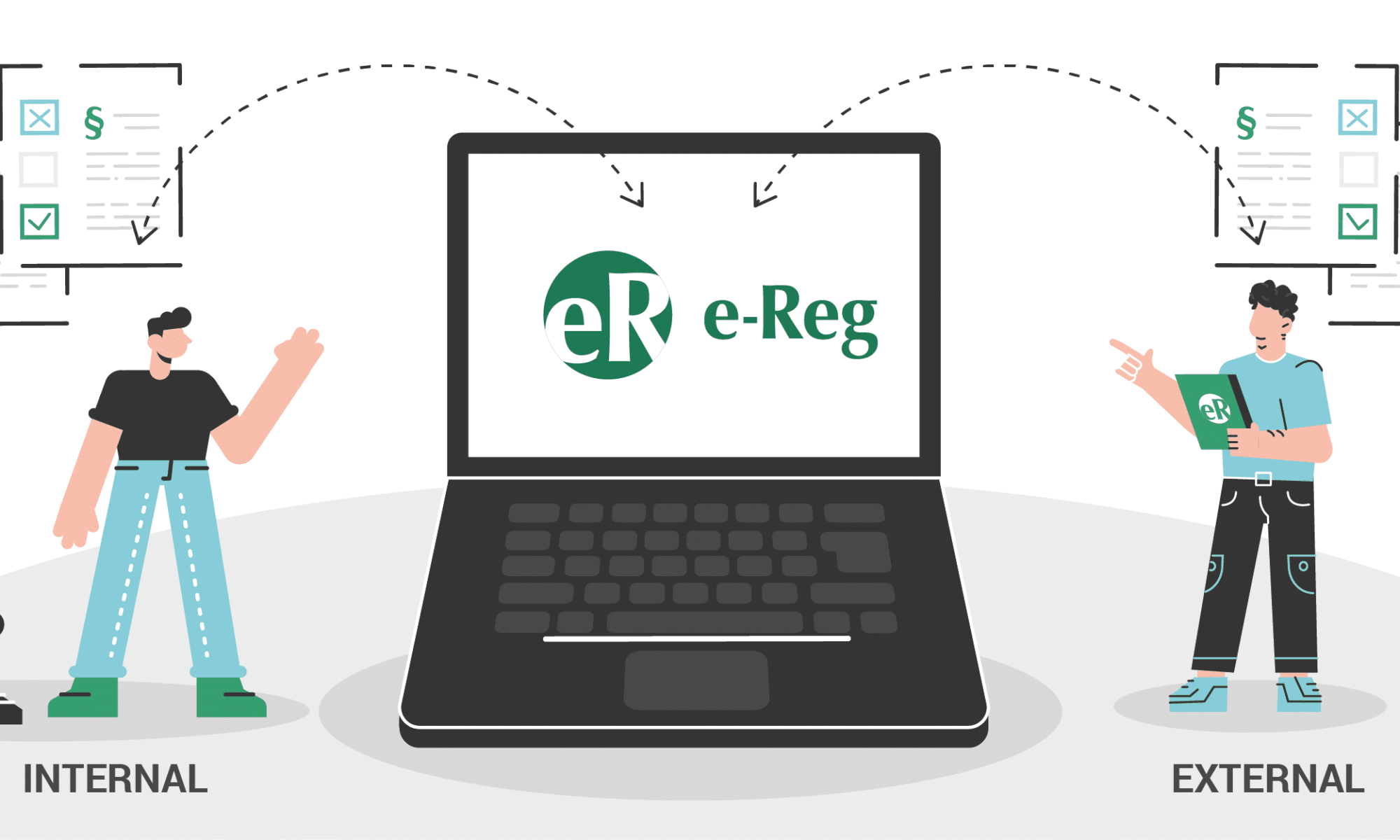

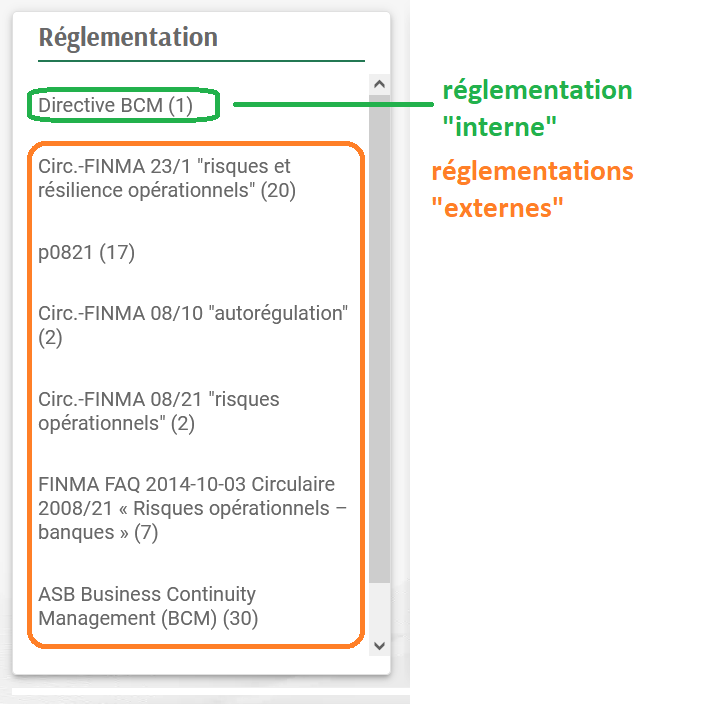

3 – Regulatory research: the advantages of e-Reg, a Swiss RegTech platform

easyReg is a RegTech company. It is dedicated to simplifying financial regulation in the Swiss banking sector.

3.1 – The mission of easyReg, a RegTech specialized in regulatory management and research

At easyReg, we’ve created a RegTech platform to help professionals working with financial regulation. Whether it’s to facilitate day-to-day tasks such as applying essential regulatory ratios or making a regulatory change, for example, e-Reg agilizes your research. Our tool digitizes all work, which improves traceability.

By adopting this technology, you :

- save time on all regulatory tasks;

- Reduce the financial cost of regulatory oversight and compliance;

- increase regulatory compliance and minimize risk.

3.2 – Examples of regulatory research using our RegTech solution

e-Reg enables companies in the Swiss banking sector to carry out their research completely digitally. Technology brings flexibility and speed to this type of task.

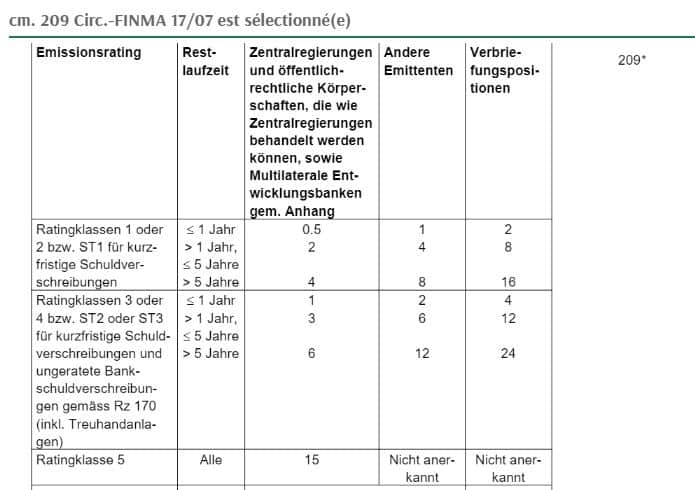

Example 1: regulatory search for “virtual currencies”

On June 30, 2023, the deadline for implementation of the new CHF 1,000 threshold for virtual currencies has approached. Search for “virtuellen währungen” to access art. 51a OBA-FINMA, which describes the requirement (2nd search result).

Example 2: Direct access to specific regulations

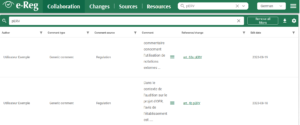

Users of the e-Reg service can enter only the number of a FINMA Circular to access it directly. For example, typing “2301” into the search engine will return FINMA Circular 23/01:

If you type “2301 47”, you will immediately obtain the text of Mn 47 of the same FINMA Circular 23/01 :

To access art. 22 a of the OBA-FINMA, enter “22a OBA-FINMA” in the regulatory search engine, without forgetting the hyphen:

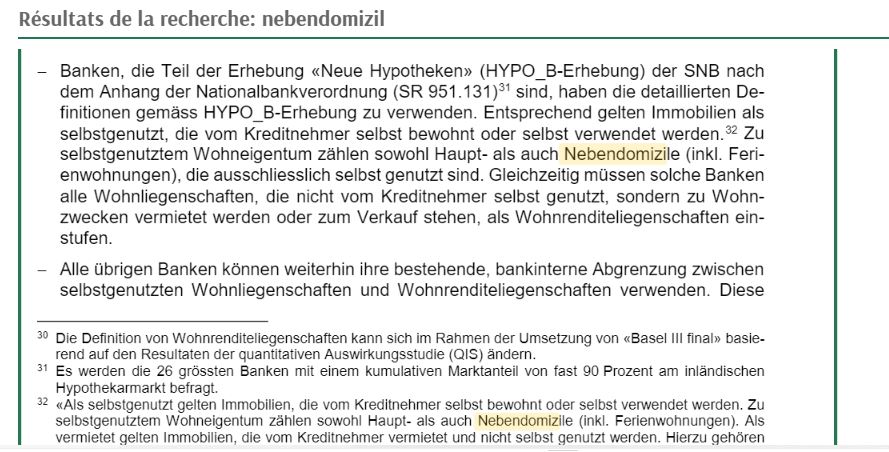

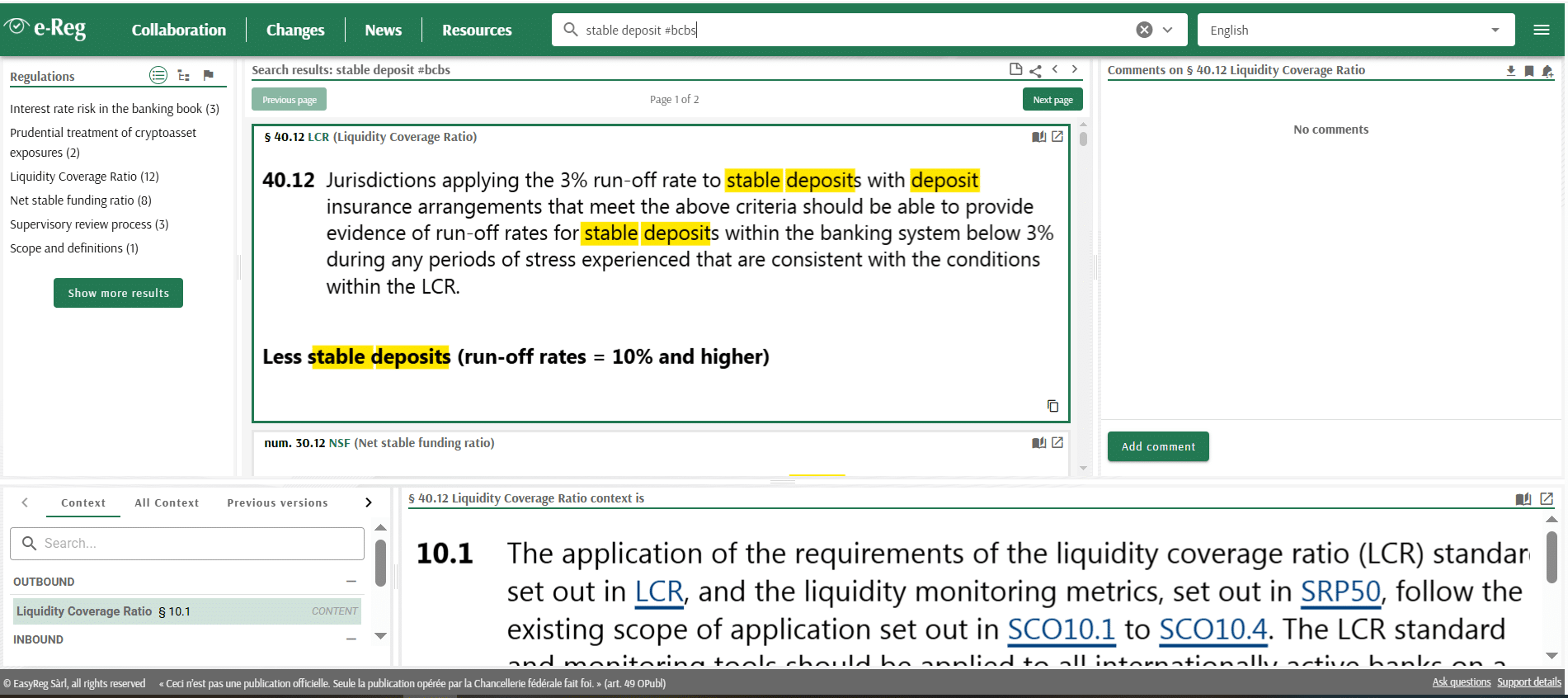

Example 3: Basel Committee

e-Reg also allows you to search across international frameworks, including Basel Committee and European regulations. For instance, searching for “stable deposit #bcbs” will instantly retrieve all relevant mentions of the term within Basel Committee documents and related files tagged with #bcbs.

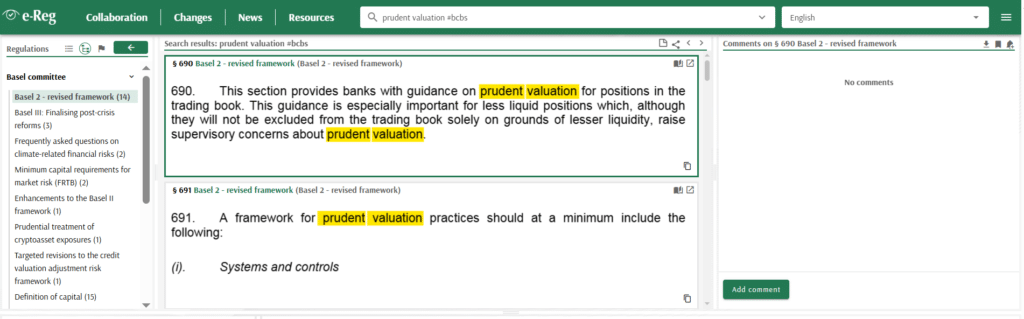

Example 4: Basel Committee

By entering “prudent valuation #bcbs”, our RegTech solution quickly isolates every reference within the Basel Committee framework, ensuring your compliance with the latest Basel Committee standards.

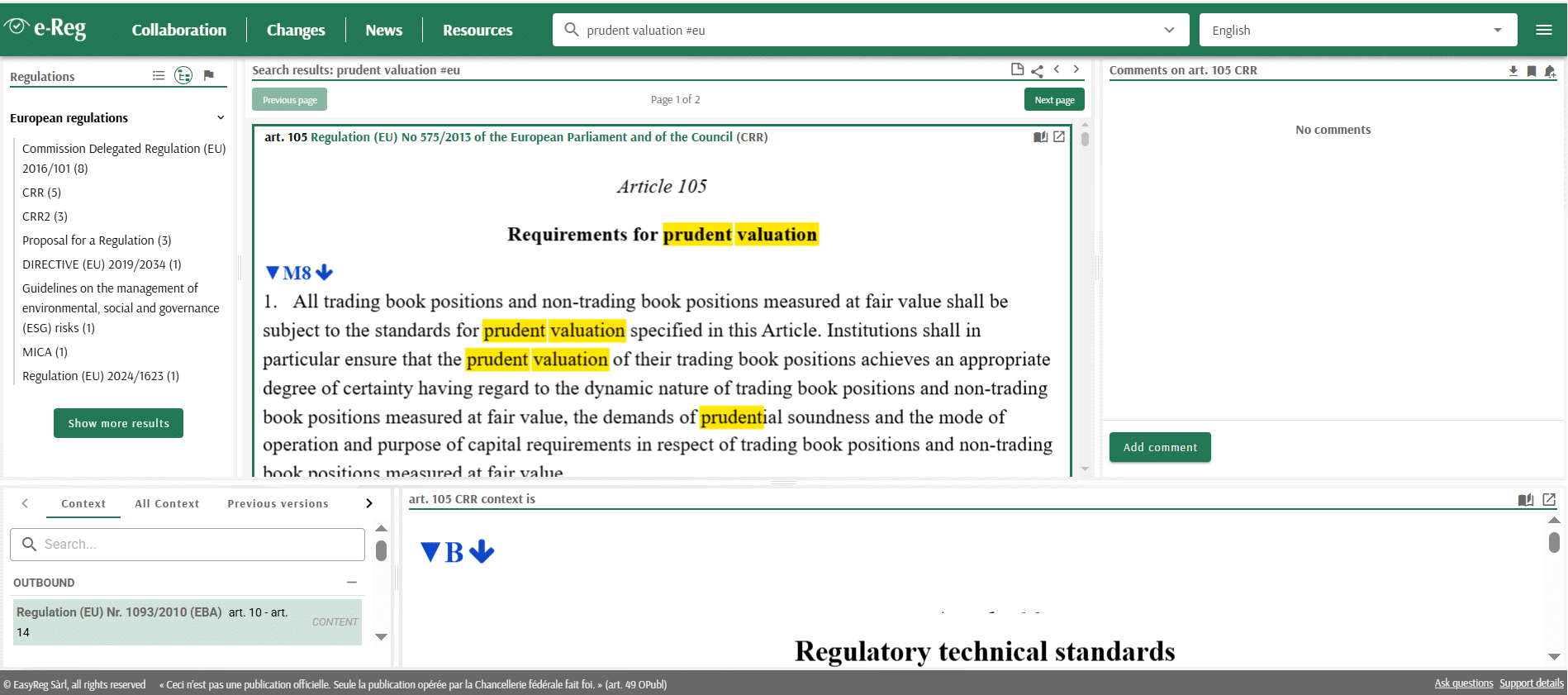

Example 5: European standards

e-Reg also streamlines access to European standards. By searching for “prudent valuation #eu”, it directly identifies key regulatory requirements, such as Article 105 of Regulation (EU) No 575/2013 (CRR).

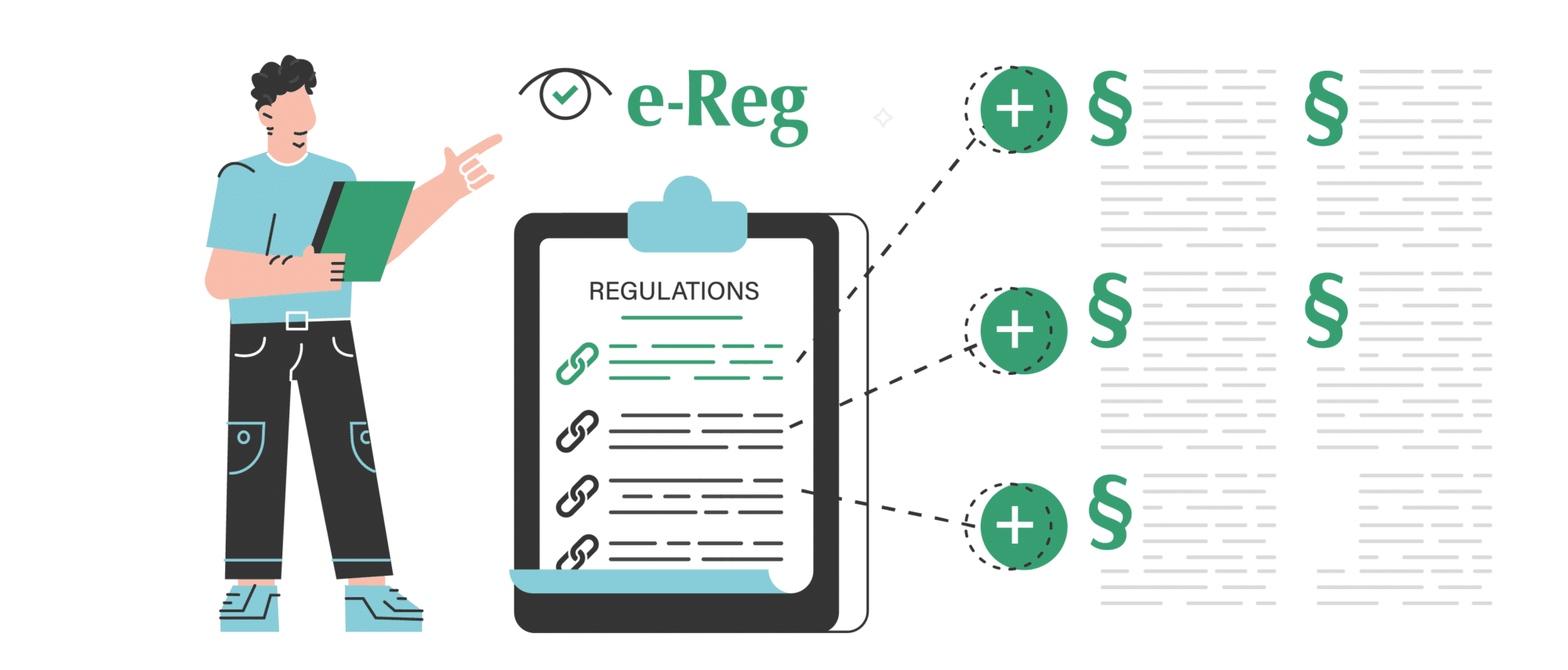

3.3 – Other services offered by our RegTech solution

e-Reg is not only a search tool, but also :

- obtaining additional information to the main regulatory search with the presence of context (additional reports and history of financial regulations);

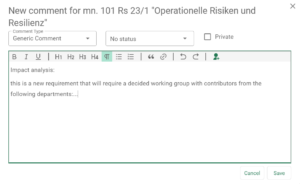

- add personal comments directly in the tool;

- share information or comments within a department (send a notification to the employee);

- collaborative project management, e.g. for a regulatory change, with task allocation and status management;

- knowledge management with traceability of data and information, with comments where appropriate;

- the provision of a multilingual library of applicable regulations, with all relevant links included in the database.

Regulatory research with RegTech makes compliance management much easier. The technology used speeds up the work, makes it more precise, and helps to pass on knowledge as knowledge. By opting for such a tool, a bank or banking consultancy gains in efficiency and reduces the cost of regulation. To convince you, we offer an online demonstration of our e-Reg platform. Make an appointment now!

👉 Sign up for our Newsletter to keep up to date with the latest regulatory news and follow any announcements of new rules or major changes.