RegTech companies offer the banking sector a wide range of regulatory and compliance management services. Some of these RegTechs, such as easyReg, specialise in tasks requiring the exploitation and analysis of regulations. Nowadays, RegTech tools of this type are able to go further than just processing standard texts. Discover the various layers of solution offered by such RegTechs , from its foundation to all possible customisations.

1 – RegTech tools: standard features for managing regulation in banks

Let’s focus first on the foundation offered by RegTech tools for managing regulatory data and information.

1.1 – What does a Regulatory Technology application do for regulatory management?

The new technologies exploited by RegTech companies combined with regulatory research constitute a real winning combo for their users. Indeed, one of the major difficulties faced banks and consultancies is the wealth and complexity of regulations.

So a Regtech solution like e-Reg offers a wide range of functions, from regulatory knowledge to collaborative information management and regulatory project management. Here is the main scope of such a tool :

- search for regulatory texts that need to be applied in Switzerland ;

- broaden the analysis by accessing the entire regulatory context surrounding the query made in the tool ;

- have access to draft changes to the texts ;

- manage and structure knowledge within a bank or law firm (comments, information sharing, regulatory libraries).

1.2 – Benefits of new RegTech-type technologies for managing banking compliance

This type of RegTech tool provides comfort and peace of mind for people whose work revolves around regulations. Let’s summarise the benefits for regular users :

- improved compliance and reduced risks of non-compliance and the associated costs ;

- time savings for financial services staff ;

- development of regulatory knowledge and skills, particularly for new recruits ;

- digitisation of tasks and traceability of regulatory analyses and research.

1.3 – What are the standard regulations generally covered by RegTech solutions like e-Reg?

Our e-Reg online platform includes a base of regulations common to all users. In a way, it is the documentary standard accessible to everyone.

Here are the databases that we integrate into the RegTech tool, representing thousands of pages of financial regulations :

- acts, ordinances and FINMA orders applicable to financial services in Switzerland ;

- explanatory reports, comments and consultation reports issued by FINMA and the FDF ;

- self-regulation, i.e. positions, recommendations and guidelines published by the AMAS and the SBA ;

- other data relating to regulatory changes, i.e. outside the laws mentioned in Art. 1 of FINMASA ;

- certain European Union regulations affecting banks in Switzerland ;

- international texts, such as those relating to Basel III final.

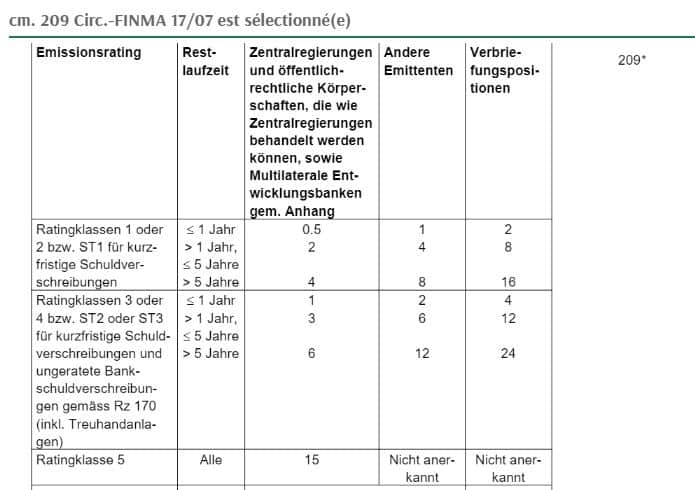

1.4 – RegTech tools and the regulatory context: example of a query on the e-Reg platform

As standard, our Regulatory Technology solution provides access not only to the results of regulatory research, but also to the entire context. This includes additional information such as additional reports and the history of financial regulations. It helps to enrich reflection and documentary analysis.

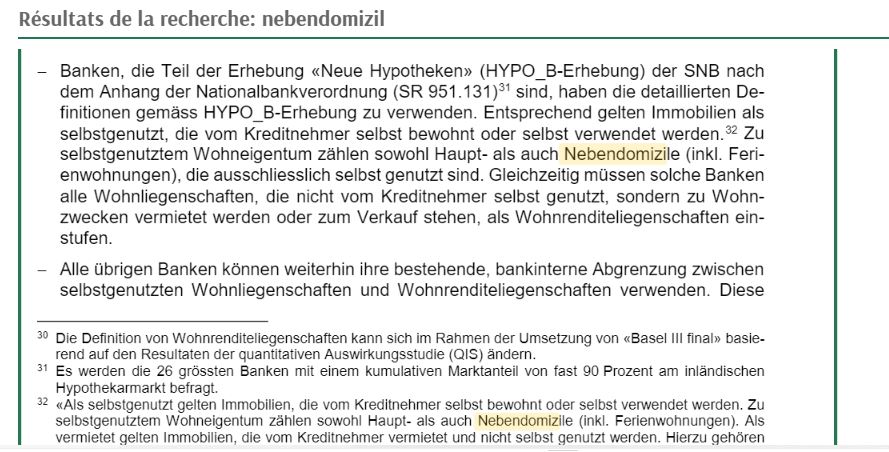

Would you like to understand what we make available to e-Reg users in banks or law firms? Here is an example of a regulatory search on the e-Reg platform for the expression “liquidity stress test”.

The window at the bottom of the screen gives access to the context, in this case the extract from the explanatory report of 4 November 2020, which deals with the subject of proportionality for stress tests in small banks.

2 – Some RegTech solutions go further in terms of regulation

In addition to this standard block offered by traditional RegTech tools, with e-Reg we provide other functionalities. We enable our customers to add additional regulations directly on the platform.

2.1 – Regulatory research: the needs of the financial services sector

Our customers express the need to centralise official Swiss regulations as well as their internal procedures or directives in one centralized place. Sometimes, for uses that are specific to their bank or their particular business, users would like to be able to consult, comment and share extracts from regulations outside of Switzerland. These may be European or international laws or regulations, for example.

2.2 – On-demand modularity of our RegTech tool

Given the needs of the financial services sector for efficient organisation and optimum compliance, we offer modularity in addition to the standard process. This ensures that users of our RegTech application have access to all sources of information centralised in a single, shared space within their institution.

2.2.1 – Possible integration of external regulations into e-Reg

The ability to add to the e-Reg regulatory information database directly within the tool widens the scope of what can be done. For example, if a customer wishes to add external regulations to meet the needs of an external establishment, this can be envisaged. In fact, the database can be expanded on demand.

2.2.2 – Possible option for a banking institution’s internal regulation module

One of the innovations we have introduced into the RegTech application is the ability to insert a financial institution’s own directives and procedures. This addition is made in a totally secure and segregated environment. As a result, employees working in the regulatory field have access to all sources of documentation, both internal and external, for each search. This simplifies collaborative project management within teams.

To find out more, read our article on this subject. It will give you a better understanding of how and why your bank’s internal regulations should be integrated into our RegTech tool.

2.2.3 – Possibility of adding to the standard if this is a plus for all users

Finally, please note that we may decide to enhance the standard base of regulations in e-Reg. This is particularly the case if a specific need expressed by a bank or consultancy is of interest to all users. That’s why our RegTech platform is scalable. What’s more, innovation is in our genes. We are constantly thinking up and deploying new functionalities, thanks to technology, in particular Artificial Intelligence (AI). One example is semantic search or vector search, a real enhancement for exploiting regulatory data.

This type of personalisation service offered to our customers in the RegTech application improves the work of our employees. With more regulations available, users are better able to comply with regulatory requirements. It’s one way of reducing the risk of non-compliance in the companies that are responsible for them. Nothing beats a personalised demonstration of the e-Reg tool. Choose a slot directly on Enrico Giacoletto’s calendy.

👉 Sign up for our Newsletter to keep up to date with the latest regulatory news and follow any announcements of new rules or major changes.