In the month of July 2022, the Federal Council and the Swiss Financial Market Supervisory Authority (FINMA) launched a consultation for the purpose of applying the latest Basel III measures in Switzerland. Do you know how the project progresses? Why is it now called Basel III Final in Switzerland (or “end game” in the US) rather than Basel III? What are “Basel IV” and “Basel consolidated”? What’s new for 2024? As Reg Tech specialists, we answer all your questions in this article and provide you with the essential documentary sources you need to know.

1 – Basel III final: what banks need to know

The Basel Committee on Banking Supervision (BCBS) aims to strengthen the global soundness of financial systems. It also aims to ensure efficient prudential supervision and good quality exchanges between banking regulators. It is managed by the central bank governors and banking supervisors of 28 countries, including Switzerland.

1.1 – Basel III and Basel III Final: strengthening banking supervision

The Basel Committee’s work resulted in the issue of rules known as standards, i.e. the minimum that banks and supervisors must apply. The reform known as Basel III is the latest standard in force. Since 2010, it has supplemented Basel II, following the global financial crisis of 2008. The member countries of the Basel Committee are committed to incorporating these measures into their national legislative frameworks.

Basel III strengthens the level of regulatory capital by raising the minimum solvency ratio to 10.5%, compared with 8% in Basel II. The reform also provides for a leverage ratio, which is the ratio between the total assets held by the bank and its equity capital. Finally, it defines the short-term liquidity ratio (LCR) and the long-term liquidity ratio (NSFR).

1.2 – Implementation of Basel III final in Switzerland

The introduction of Basel III final into law includes a revision of the Ordinance on Capital Requirements (OFR). It also includes a complete overhaul of the texts detailing the implementation of the OFR. Circulars 2013/01, 2015/03, 2008/21 (equity capital section), 2017/07, 2016/01 and 2008/20 are repealed. New ordinances of the Swiss Financial Market Supervisory Authority replace them (see below).

1.3 – When will Basel III come into force in Switzerland?

The consultation launched in July 2022 by the Federal Council and the Swiss Financial Market Supervisory Authority was completed in 2023. The amendment to the Capital Adequacy Ordinance, adopted by the Federal Council on 29 November 2023, will come into force on 1 January 2025.

FINMA’s press release of 27 March 2024 also announces the publication of the ordinances to implement Basel III final in Switzerland. These will come into force on 1 January 2025, at the same time as the corresponding changes to the Capital Adequacy Ordinance.

We list all these regulatory changes in a later part of the article, updated in April 2024.

2 – Why talk about Basel III final?

The Basel Committee on Banking Supervision refers to the Basel III reform. However, the second part of the package is actually called Basel III Final.

2.1 – The Basel Committee adopts an initial set of measures

In the wake of the 2008 financial crisis, the shortcomings of the Basel II standard came to light. In 2010, the Basel Committee quickly approved a new regulatory framework for banks and financial institutions. The first version, published in December 2010, was updated in June 2011. However, this is only the first part of the reform requirements. For Switzerland, these initial measures are detailed in the communication from the Federal Department of Finance (FDF) dated 1 June 2012.

2.2 – The other Basel III reforms will be incorporated into Basel III final

On 7 December 2017, the BCBS finally published the final applicable Basel standards. As a result, this section on strengthening banks’ capital according to risk is called Basel III final, as opposed to the first wave of reforms, which dates back several years.

The provisions of Basel III final include risk weightings with various ratios based on company ratings. The standards also incorporate a new approach to operational risk. In Switzerland, Basel III Final will lead to the July 2022 consultation launched by the FDF and FINMA.

2.3 – Basel IV or Basel III final: the Basel Committee has chosen

During the work to implement the Basel III measures, several years after the first series of reforms, two terms emerged: Basel IV and final Basel III. In the end, the BCBS chose Basel III final, as indicated in its 2017 publication.

3 – Regulatory texts and other information on the Basel III final reform in Switzerland

Here is some other useful information and in particular the new ordinances.

3.1 – Where can I find the key texts?

Are you looking for the key articles on this banking supervision reform? Take a look at the following sources:

- The Basel Committee published the document ‘ Basel III: Finalising post-crisis reforms’ in December 2017, which contains all the elements of Basel III ;

- FDF and FINMA publications on the consultation on the implementation of Basel III final in Switzerland, which opens on 4 July 2022 ;

- Amendment to the Capital Adequacy Ordinance (CAO) on 29 November 2023 ;

- FINMA press release dated 27 March 2024 for the ordinances relating to the implementation of Basel III final, with a view to the effective application of the OFR following its revision.

3.2 – List of new ordinances

You will find all the documentation (draft ordinances, explanatory reports, information on the hearing, etc.) on the FINMA website. Go to the archive of hearings completed in 2022.

The following FINMA ordinances were published at the beginning of 2024:

- TBEO-FINMA (the Ordinance on Trading book and Banking book and Eligible capital of banks and securities firms) relates to the trading book and the bank’s book, as well as the capital taken into account of banks and securities houses. It replaces FINMA Circular 2013/1 ‘Recognised own funds – banks’.

- LROO-FINMA (the Leverage Ratio and Operational Risks of Banks and Securities Firms Ordinance) relates to the leverage ratio and operational risks of banks and securities firms. It replaces FINMA Circular 2015/3 ‘Leverage ratio-banks’ and the parts of FINMA Circular 2008/21 ‘Operational risks-banks’ that are still in force.

- CreO-FINMA (the Ordinance on the Credit Risks of Banks and securities firms) deals with the credit risks of banks and securities firms, replacing the former FINMA circular 2017/7 ‘Credit risks-banks’.

- MarO-FINMA (the Ordinance on the Market Risks of Banks and securities firms) deals with the market risks of banks and securities firms. It replaces FINMA Circular 2008/20 ‘Market Risks – Banks’.

- Finally, DisO-FINMA (the Ordinance on the Disclosure Obligations of banks and securities firms) concerns the disclosure obligations of banks and securities firms. It replaces FINMA Circular 2016/1 ‘Publication – Banks’.

3.3 – What is the Basel consolidated format?

In April 2019, the Basel Committee on Banking Supervision (BCBS) brought together the various global standards for banking regulation and supervision. The aim of Basel Consolidated is to bring together all the regulatory provisions and to clarify and simplify the existing standards, without adding any new ones. The approach is explained in this document concerning Basel Consolidated.

4 – How can e-Reg help you with Basel III?

In the face of these ongoing regulatory changes, it is vital to keep up to date on a regular basis. As a financial services professional, you are looking for the right information, accurate and reliable, at all times. That’s where e-Reg can make your job a lot easier.

4.1 – e-Reg a RegTech solution for your search for regulatory documentation

Our aim at easyReg is to simplify your regulatory work. We offer you a service in SaaS mode (Service as a Software) so that, thanks to our search engine, you can access the exact information you need. Whether you are a Swiss financial institution, a law firm or a consultancy, this tool is specifically designed for you.

Instead of searching through Swiss regulations and Basel Committee documents, use e-Reg to obtain not only the precise text, but also its context. It’s a real lever for your analyses and the management of your documentary needs. We also provide you with all the other regulatory information relevant to your subject. You can also consult the comments of your colleagues on these same texts.

4.2 – Search examples for Swiss capital adequacy regulations

There’s no better way to understand our Reg Tech solution than to look at a few concrete cases.

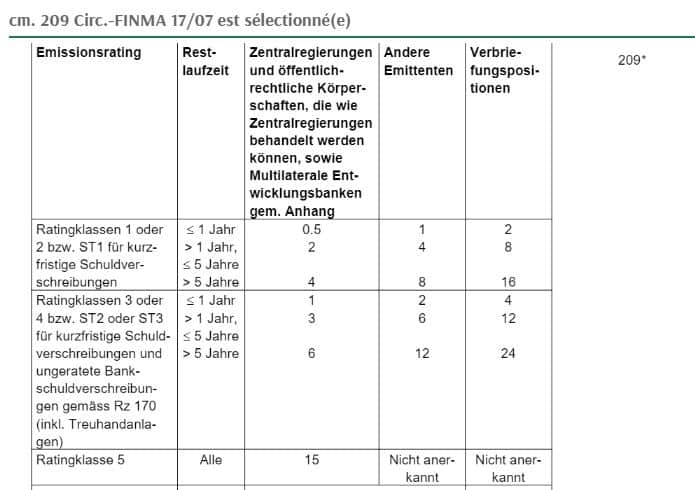

Example 1: regulatory discount

Enter the expression ‘regulatory haircut’ (Sicherheitsabschläge) in our e-Reg search engine:

![]()

You will be taken directly to the table of current and future regulations:

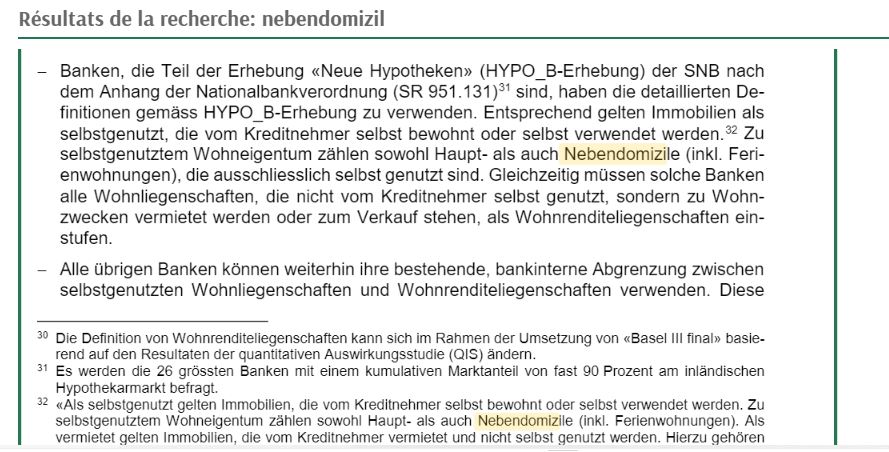

Example 2: treatment of second homes in the calculation of equity capital

Do you have any doubts about how to calculate equity capital for second homes? Proceed in the same way by entering ‘second homes’ in the e-Reg engine.

You’ll get the following information:

Example 3: Basel III regulations

Our e-Reg platform includes a ‘changes’ module. Here you will find, for example, the item ‘Basel III final’ with access to :

- an analysis of the main impacts of these new regulations applicable in 2025 ;

- clickable references to key sources of regulatory information ;

- the ability to drag reference files into the tool, along with notes and comments.

This example of evolving regulations shows how important it is to have up-to-date, reliable information at all times. At easyReg, this is our business. To find out more about how our platform can help you with your document searches, arrange an online demo of our e-Reg tool.

👉 Sign up for our Newsletter to keep up to date with the latest regulatory news and follow any announcements of new rules or major changes.